In banking, failure isn’t an option. A single bug in transaction logic costs real money, sometimes millions. A compliance gap creates regulatory nightmares. A fraud detection system that misses patterns puts customers at risk.

This is why “moving fast and breaking things” doesn’t exist in fintech. Code, all API calls, and all data changes must all be correct at day one.

That’s where AI-powered QA comes in. It’s not hype. It’s a necessity.

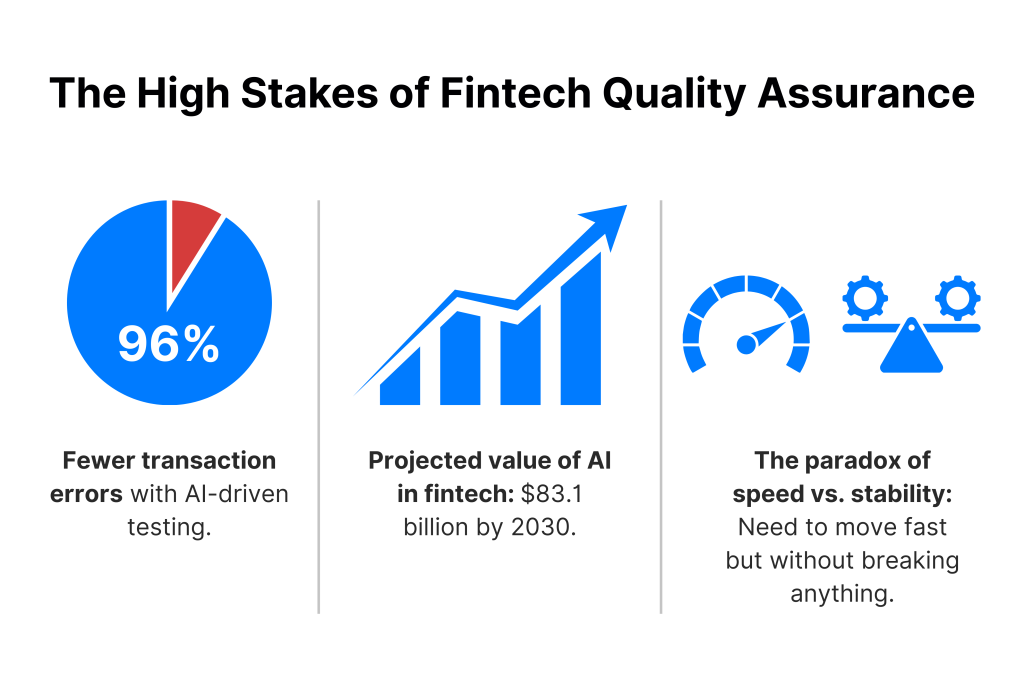

The High Stakes of Fintech Quality Assurance

Banks don’t get second chances. When Eurobank, Wells Fargo, and Metro Bank embedded AI agents into their core systems, they weren’t experimenting. They were hoping that the systems would be able to process verifiable transactions without errors.

The numbers back them up. Organizations using AI-driven testing see 96% fewer transaction errors. That’s not marginal improvement-that’s the difference between a stable platform and a liability.

But here’s the tension: fintech moves at lightning speed. Consumers desire fast payment, real-time fraud checking and instant loan approval. By 2030, AI in fintech may be valued at $83.1 billion. Things are really hard. But all new features need to follow strict rules that will impress other industries.

This creates a paradox. You need to move fast. But you can’t break anything.

AI-powered QA solves this by catching defects before they reach production. It validates complex workflows. It makes sure everything follows the rules. It does the work of hundreds of manual testers in a fraction of the time.

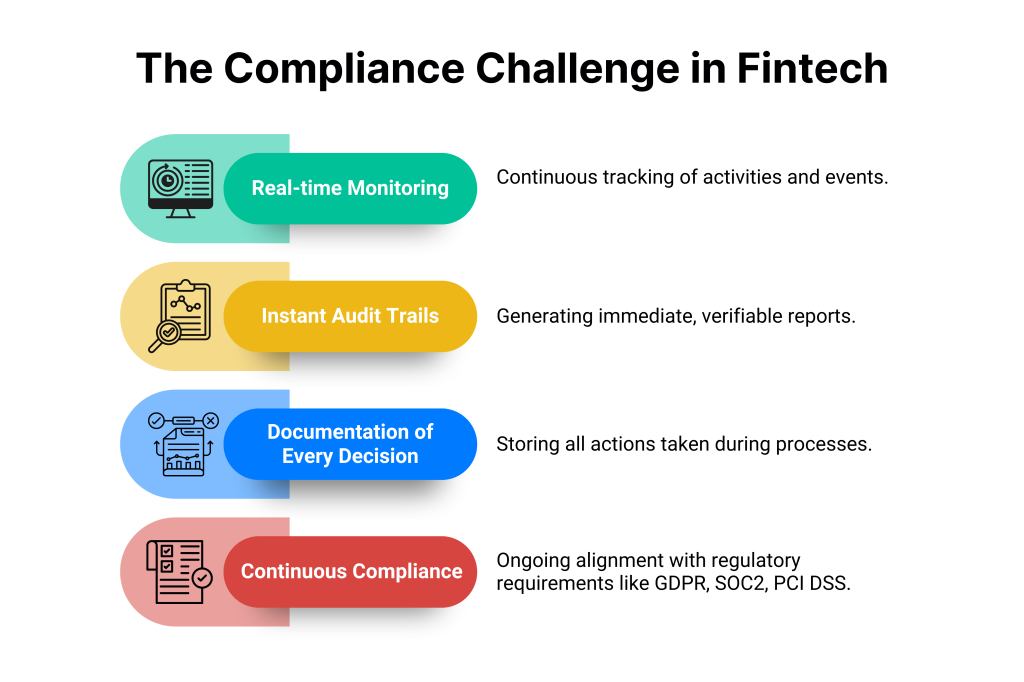

The Compliance Challenge: Automating What Used To Break Teams

Traditional compliance was simple. You hired auditors. They came in once a year. They reviewed documentation. You fixed whatever they found. Then you waited 11 months to hear from them again.

The old paradigm is no longer operable.

Continuous compliance is now desired by regulators. They require:

- Real-time monitoring

- Instant audit trails

- Documentation of each decision

GDPR, SOC2, and PCI DSS are not checklists that can be merely ticked. They’re ongoing obligations.

Most banks handle this by throwing people at it. Compliance teams work nights updating spreadsheets. Risk officers manually map controls. Developers scramble to find evidence when auditors ask questions.

AI changes this entirely.

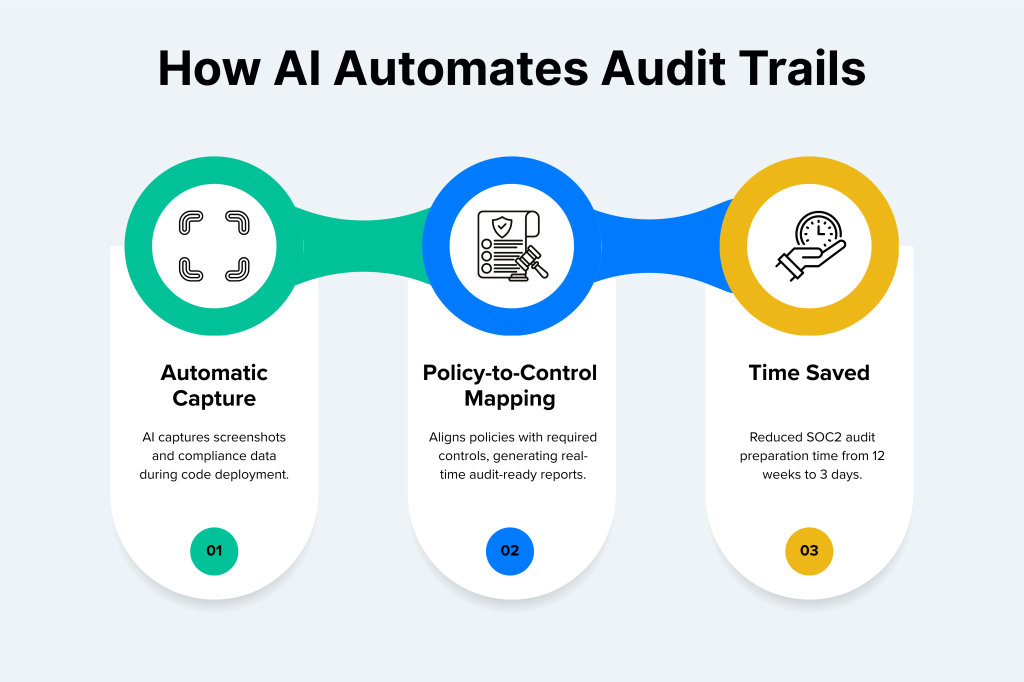

Automating Audit Trails for Every Release

AI compliance tools can now automatically connect policies with controls and extract evidence in tools like AWS, GitHub, and Jira and generate audit-ready reports in real time. The results are striking.

One fintech firm reduced SOC2 audit preparation from 12 weeks to 3 days.

Here’s how it works in practice:

An AI agent will automatically capture screenshots, record compliance, and compare it to required controls when you deploy code. The evidence is already assembled and labeled by the time your auditor inquires of you.

No more emergency document hunts. No more compliance crises on Thursday night before a Friday deadline.

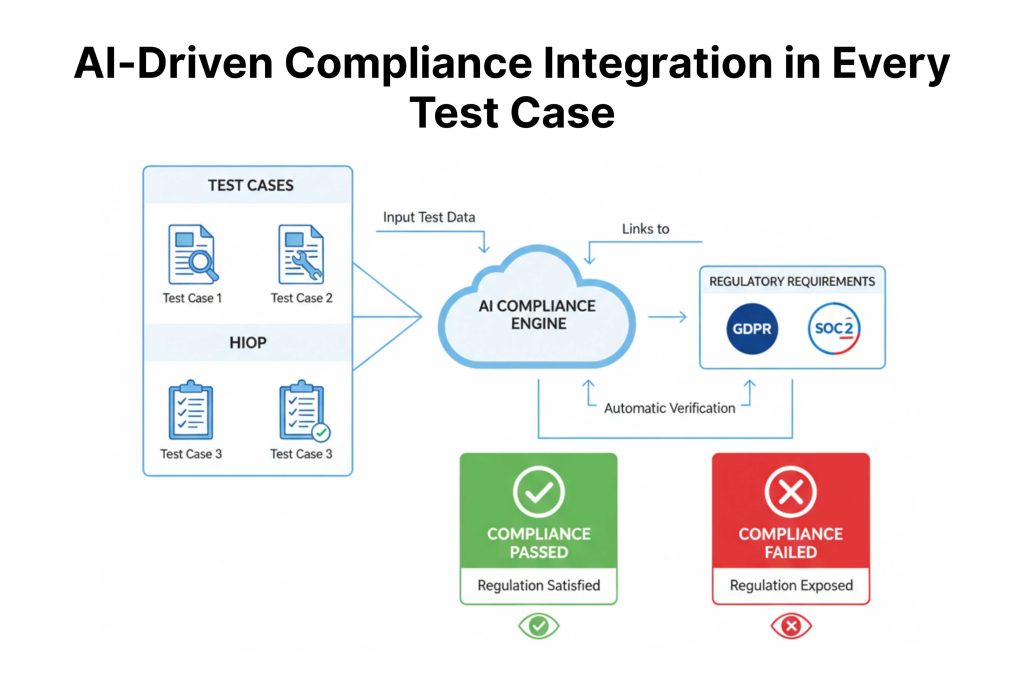

Regulatory Alignment Built Into Every Test Case

GDPR compliance isn’t just about data protection-it’s about proving you protected data. SOC2 isn’t just about security controls-it’s about demonstrating those controls worked.

Modern AI QA does something older tools couldn’t: it ties every test case back to specific regulatory requirements. When a test passes, you know exactly which law it satisfies. When it fails, you know precisely where you’re exposed.

This transforms compliance from a back-office problem into a core product requirement. Developers write code. Tests run. Compliance is automatically verified. No handoff needed.

The benefit? AI reduces manual compliance work by up to 80%. That’s not automation theater. That’s your team actually getting their lives back.

Where AI Actually Delivers Value in Banking

Not every AI marketing claim deserves your attention. But in specific areas, AI solves problems that humans simply can’t scale.

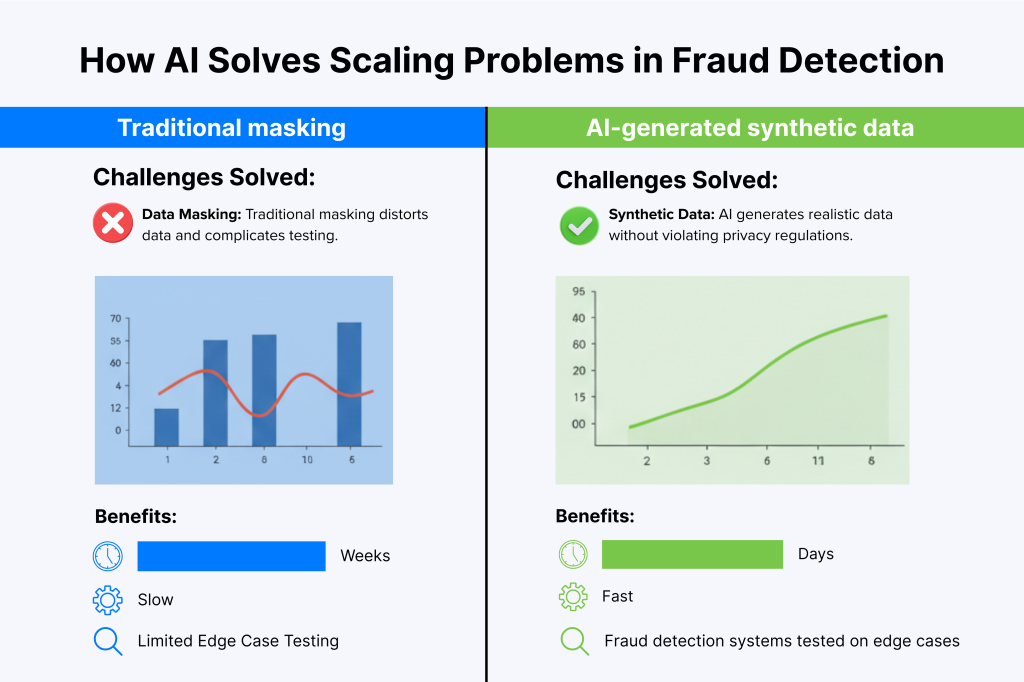

PII Data Masking & Synthetic Data: Testing Without Risk

This is a typical issue: fraud detection should also be tested with real customer data. We would not be able to duplicate the production databases as it goes against GDPR, CCPA, and other privacy regulations.

So teams are forced to work around:

- Manual masking that distorts data

- Slow approval processes

- Restricted access that kills innovation

Synthetic data fixes this.

AI is now able to generate artificial datasets that look, behave, and perform as authentic customer data, without the information of actual people. The counterfeit data retains the identical statistics that render it convenient for testing. They pass compliance because they contain no actual PII.

The impact is immediate:

- Data approval timelines compress from weeks to days

- ML models train faster

- Fraud detection systems can be tested against edge cases that rarely appear in production

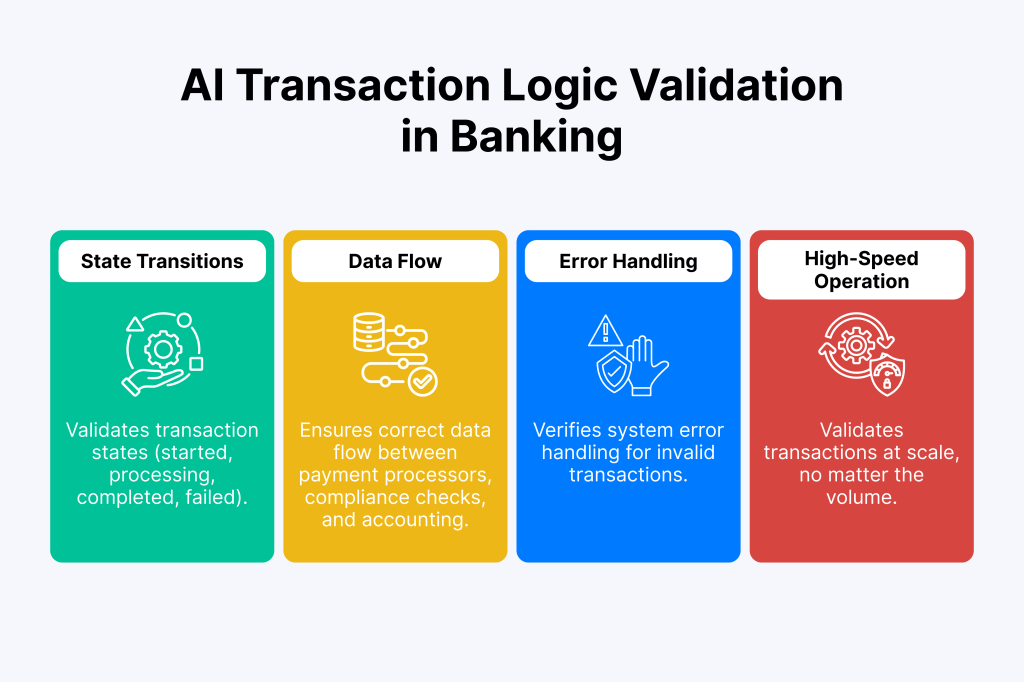

Transaction Logic Validation: Ensuring Complex Workflows Work Across APIs

Banking isn’t one system. It’s dozens of APIs, payment gateways, lending platforms, and core processing systems all talking to each other simultaneously.

A single transaction might touch five different systems. If any of them fail, return incorrect data, or don’t handle edge cases, the whole operation breaks down.

Manual testing can’t scale to this complexity. There are too many permutations. Too many failure modes. Too many race conditions are hiding in the details.

AI-powered transaction testing works differently. It doesn’t test happy paths only. It validates:

- State transitions appropriately through all possible transaction states: started, waiting, being worked on, finished, and failed

- Correct flow of data between payment processors, compliance checks, and accounting records

- Error handling so the system remains operational when transactions are invalid

- High-speed operation, no matter the number of trades occurring simultaneously

The result is that what would have been done in weeks of testing by hand can be checked in a few hours.

The Black Box Problem: Why Auditors Don’t Trust Hidden Decisions

Here’s where AI in banking gets tricky.

Regulators understand traditional code. They can audit a loan approval algorithm because it’s built on rules they can see. They can verify a fraud detection system because someone wrote the logic down.

But drop a neural network into an AI agent, and things get opaque fast.

The model says, “deny this loan.” It has 94% accuracy historically. But the auditor asks: Why did you deny this specific applicant?

If you can’t explain the decision, you have a problem. Not just a compliance problem-a legal one.

This is why explainability has become mandatory in regulated finance.

Building Systems Auditors Can Actually Follow

Explainable AI doesn’t mean dumbing down your models. It means building transparency into how they work.

The EU AI Act, GDPR, and AML regulations all require institutions to explain significant AI decisions. That’s not optional. It’s the law.

Modern AI QA platforms handle this by:

- Maintaining complete audit logs of every decision, with full traceability back to inputs

- Using interpretable techniques like SHAP values and feature importance scores that explain which factors drove each decision

- Storing decision rationale so compliance officers can review why the system flagged a transaction

- Enabling human review loops where AI recommendations are checked before final decisions

One compliance firm reported that explainable AI systems achieve 99.2–99.8% accuracy on compliance tasks, higher than manual processes, which typically hit 85–90%.

The audit trail becomes your proof. Every decision is documented. Every factor is recorded. Regulators can follow the logic from input to conclusion.

Security & Privacy: Why On-Premise AI Exists

In the field of fintech, it may seem dangerous to take your own algorithms to the cloud.

It’s not paranoia. It’s a business reality.

A fintech company that trains its fraud detection model on its API could theoretically have that model extracted by a clever competitor. The algorithm becomes reverse-engineered through repeated API calls. Millions in R&D disappear into someone else’s product.

This is why large banks increasingly run AI models on-premise.

Keeping Proprietary Code and Sensitive Data Internal

On-premise AI isn’t about rejecting cloud technology. It’s about controlling what leaves your building.

Your fraud detection logic stays internal. Your customer transaction patterns stay internal. Your risk models stay internal.

Instead, deploy the AI engine to your data center, with your own security, monitoring, and audit history.

The compliance benefits are immediate:

- Sensitive data never touches external servers

- You can’t accidentally leak what never leaves your walls

- Complete datasets enable faster model training-no redaction or masking needed

- Models train faster, accuracy improves, and security reviews happen internally

For high-sensitivity work like fraud detection or credit scoring, this matters enormously. On-premise deployment eliminates a whole category of risk.

Shift-Left Security: Making AI Safe Before Production

Traditional security testing happens at the end of development. Code gets written. Features get built. Then, security teams spend weeks finding vulnerabilities before release.

In banking, that’s too slow.

Shift-left security means embedding safety checks at every stage, starting when data enters your system, not ending when code reaches production.

Testing Data, Models, and Systems Before They Reach Users

There are three primary failures of AI systems:

- Bad data hurts the model: Training bad, malicious, or biased data makes the model learn bad patterns

- Weak models do not work under stress: They perform well with clean test data but fail on real-life variations, trick cases, or cases the model has never been trained on

- Faulty systems spurt confidential logic: Fuzzing attacks can fool the model to reveal its decision rules. Attacker-crafted inputs disclose the functionality of the model

Each of them is dealt with by shift-left security.

Data Integrity Checks:

- Statistical tests identify data poisoning before training

- Distribution analysis points out suspicious inputs

- Consistency checks identify conflicting examples

Adversarial Testing:

- Intentionally attempts to misuse the model

- Fast Gradient Sign Method and Projected Gradient Descent attacks model how real attackers can misuse your fraud detection or credit scoring models

Semantic API Fuzzing

- Verifies whether the model can handle unexpected yet valid requests with ease

- Example scenarios: loan request by an applicant of 200 years old, transactions with impossibly large amounts, requests that reveal business logic errors

Outcome: A fintech firm reduced manual QA efforts by 40% and identified twice as many bugs in the logic prior to product release using shift-left security.

Load Testing for High-Frequency Trading: Handling Real-World Chaos

High-frequency trading systems live on the edge.

Thousands of transactions per second. Microsecond latencies. Market volatility that creates sudden spikes in order volume. A one-millisecond delay costs real money.

Testing these systems means simulating realistic chaos, not clean test scenarios.

Stress Testing the System Until It Breaks

Most load testing follows a script: ramp up traffic, measure response times, publish a report.

For trading systems, that’s insufficient.

Realistic testing means:

- Patterns of loading that gradually increase pressure, discovering where it ruptures

- Micro-burst load, which replicates actual market behavior, sudden bursts and quiet intervals

- State transition testing to ensure orders are properly transferred between pending → processing → completed states

- Consistency validation that the same trade isn’t done twice, amounts don’t change mid-transaction, and the ledger remains correct

The present load generators are capable of supporting more than 70000 transactions per second on a single server.

However, consistency is greater than speed. Any system that is dependably providing 0.8-milliseconds latency is preferable to one that is intermittently ranging over 0.3-2.1ms, as traders must have confidence in their systems.

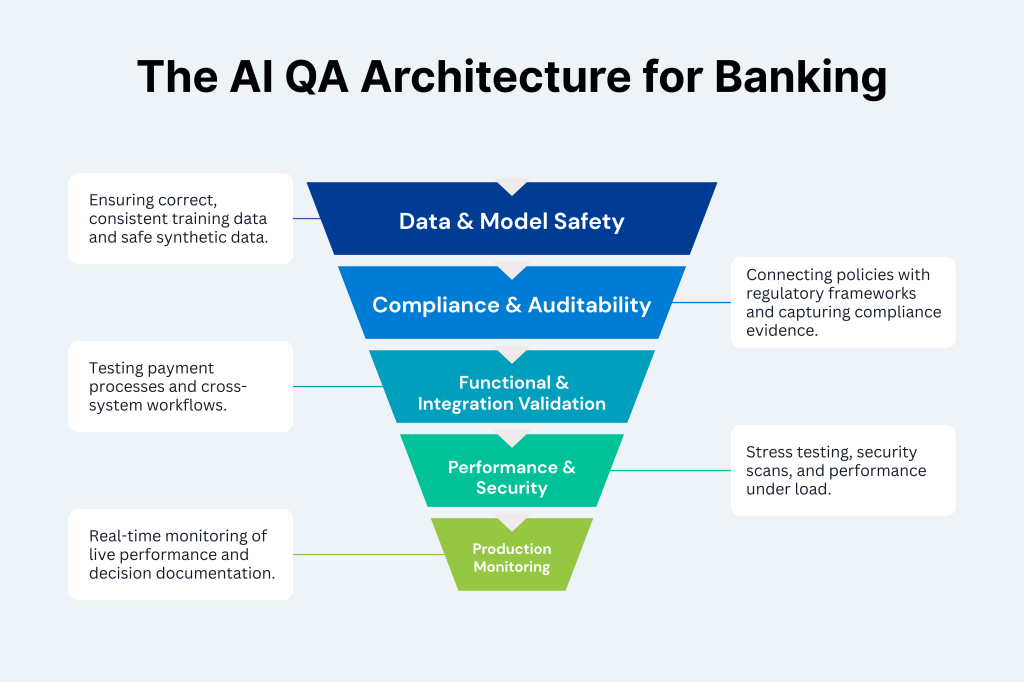

Bringing It Together: The AI QA Architecture for Banking

A complete AI QA solution for banking isn’t a single tool. It’s layers of validation working together.

Layer 1: Data & Model Safety

- Develop synthetic information that won’t harm privacy

- Assure that the training data is correct and consistent

- Check the models to ensure they can accept difficult or deceptive inputs

- Discover discriminatory trends in the treatment of various customer categories

Layer 2: Compliance & Auditability

- Auto-connect the regulations of the system with government frameworks

- Collect evidence everywhere on your technology stack

- Maintain records on why decisions were taken

- Continuously ensure compliance monitoring

Layer 3: Functional & Integration Validation

- Test the entire payment process with all payment interfaces

- Check that system states evolve correctly

- Ensure cross-system workflows are functioning properly

- Check system response to errors and the ability to undo changes

Layer 4: Performance & Security

- Check the system with a large number of trades

- Evaluate the system in harsh market environments

- Detect security threats at the initial stages with automated scans

- Ensure APIs have agreed-upon rules that are consistent

Layer 5: Production Monitoring

- Monitor and observe live performance

- Test model accuracy to ensure nothing surprises the model

- Document every decision taken

- Receive notifications about anything out of the ordinary

Why This Matters Now

Regulators are getting serious about AI. The UK Financial Conduct Authority launched AI testing environments. The EU is expanding AI Act oversight. Every major financial regulator is asking: Can you prove your AI systems work safely?

Banks that answer “yes” with auditable evidence move faster. They get regulatory approval quicker. They ship features with confidence.

Banks that skip AI QA will face delays, audit failures, and the lingering fear that the next bug could be a million-dollar mistake.

The cost of inaction isn’t just missed opportunities; it’s competitive obsolescence. By 2026, AI agents will be standard in core banking systems. Firms without proper QA will be the ones explaining failures to auditors, not the ones shipping new products.

Conclusion: Risk Mitigation in the Age of Instant Payments

There is no need to tie everything together.

Start with your biggest risk. In the case of certain banks, that may be fraud catching. To others, it may be doing things by the book. In the case of fintech companies, it can be the processing of payments.

Select a significant workflow. List the test cases. Put security checks early. Add continuous monitoring.

Test the outcomes: quicker releases, fewer bugs, less auditory difficulties.

Then grow it.

Those companies that begin to use AI QA early do not seek fame. They simply desire to remain competitive. Each release is auditable. All transactions are verified. All the decisions are explainable.

That is the new banking standard. Anything else is nothing but an inconvenience.

Give Kualitee a try for 14 days, and you don’t need a credit card. Check out how AI QA can make your banking tasks easier and find problems before they go live.